August 2026

The summer of 2026 is now well underway, and it’s been a notable season, not just for the heatwaves. For some, memories of the summer heat of 1976 spring to mind.

The anticipated fast-track to Prime Minister of Andy Burnham MP was completed in July along with his partial move to Number 10 North, although some enjoyed the distraction from politics of the world football championships. With the political party conference season starting in the autumn, it will be interesting to see the new positions that parties take as we all look forward.

There are many events ahead for the balance of the year, with a UK Budget now confirmed to be on 28 October, of course now to be delivered by our new Chancellor, John Healey MP. Also shortly afterwards, in early November we have the mid-term elections in the US which may change the current balance of political power in America. As normal, we will aim to keep you updated on any Budget changes post the announcements.

With the war in Iran and the Middle East still smouldering, it may well take some time for the economies of the world to recover and for price inflation to be brought under control. An example in the UK is the next energy price cap announcement, which is a few months ahead, and some predict this may well be a significant uplift when announced. Many individuals are old enough to be acutely aware of the UK economy in the 1970s and early 80s and there is a real feel of the same position now. This adds to the economic fears for the future on many fronts, but particularly at the moment inflation.

Notably in our experience, there does seem to have been a shift in thinking from many, now with a closer eye on wealth preservation for themselves, rather than an increase in wealth transfer to other generations. Some gifting is still ongoing, via lump sums or through regular / annual gifts; however, many are feeling the real pressures of inflation on household budgets. The headline rates of inflation belie the real rates felt at the petrol pumps and in the supermarket.

The current political malaise and uncertainty is not helping. Further changes in legislation may come through that might see yet more changes to pensions and investments, as we have seen with the forthcoming introduction of IHT on pensions from April 2027. This has been a notable concern for some clients and taking advice early is usually worthwhile.

From a communication perspective (as per this page), keeping the website and client / connections relevant to the current ‘vibe’ of the economy is both helpful and in some cases reassuring. For investors, we have the offset of the need to meet higher costs with many equity markets seeing firm gains over the last year or so. Considering these and how they can be used if needed can offer some alleviation to any fears at hand. This is not always the case but is an example and a benefit of regular reviews.

The new tax year 2026/2027 is now in full swing and there is much to consider globally, not least with the very recent events in the Middle East. As observations, some global areas (America / Germany / Japan as examples) are deliberately ‘running hot’ on their economies which in turn is fuelling some equity markets and we do not expect these positions to change in the near term although, as noted above, there are no guarantees. Russia and Ukraine are still firmly in the news having reached into the fourth year of hostilities, and with what appears to be the stalling of negotiations to bring the conflict to an end. Increased spending on (national and collective) defence has been agreed over the next years, and it almost has a feel of returning to the ‘cold war’ of decades ago.

Economic data from home and abroad

Later July 2026 saw the Office for National Statistics (ONS) confirm that the Consumer Prices Index (CPI) falling to 2.6% in June 2026. Transport costs, particularly diesel fuel prices, fell away and other areas, such as food prices reduced. The Bank of England target for UK inflation remains unchanged at 2.0%, and inflation is remaining above this level.

As a note, US inflation was elevated in the most recent statistics - consumer prices (before seasonal adjustment) increased to 4.2% over the 12 months to May 2026. It is thought that this does reflect the pressures associated with the recent conflicts in the middle east.

The Bank of England maintained the base interest rate at its June 2026 rate decision meeting, holding at 3.75% again. Earlier in the year, it was thought that March or April might have been a time to reduce rates (it was a close decision in February 2026). With the indicated proposals towards the end of June to end the conflicts in the middle east, oil and energy prices have reduced, although restoring supply positions may take some time, which may keep upward pressure on UK inflation rates (as we have seen in America, noted above). Also in its June meeting, and under the new leadership of Kevin Warsh, the US Federal Reserve continued to hold the base rate to a range of 3.50-3.75%.

It should be noted that higher interest rates are good news for savers, and some savings accounts are offering 4.25% - 4.50% pa gross plus. Look out for the AER rate pa (Annual Equivalent Rate) which show the real rate of interest being provided. Of course, higher interest rates are not so good for variable rate borrowers, and the days of cheap borrowing for individuals and nations are over, certainly in the shorter term.

As you might anticipate, many financial thoughts will be UK focused; however, the world is now a small place and many of these economic factors are occurring globally, as we enter a new era of higher costs (particularly energy), inflation, interest rates and the like. Increasing numbers of global conflicts remain constant at this time, along with applications of US tariffs.

We have looked at some of these points below.

GBP / US dollar

Many readers will know that exchange rates can vary for many economic reasons. For some, it may only become apparent when purchasing foreign currency for a holiday or visit abroad. The current indicated exchange rate is $1.35 at the time of writing (05 August 2026), still an elevated rate in recent times.

UK Net Public Sector Gross Domestic Debt v GDP

It is noteworthy that net public sector debt has consistently run for some time at approximately 94%-100% of UK monthly GDP (gross domestic product) (source: Office for National Statistics / ONS). June 2026 saw a decrease, with the statistics showing the provisional estimate as 94.9% and remains at levels last seen in the early 1960s. Some will not want to see this level (and its associated interest costs) rise.

The ONS notes that UK GDP in the three months to May 2026 grew by 0.7%. This follows a growth of 0.8% in the three months to April 2026 (revised up from a growth of 0.7% in our previous publication) and an unrevised growth of 0.6% in the three months to March 2026.

Many global trading areas are revisiting their growth forecasts due to the recent conflict in the Middle East and the inflationary rises expected to occur due to energy / oil price rises.

Markets factor in most things

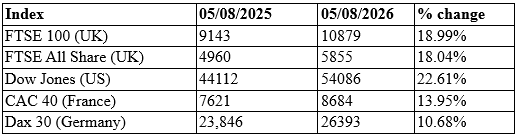

Turning to the recent market position, many individuals may refer to the value of their pension or ISA arrangements as a reference point to how markets are moving. We all know that the value of funds can fall as well as rise, and we have seen some volatility this year, although alongside positive returns from some global equity markets in both 2025 and 2026. Volatility is not uncommon, and this can be triggered by global economic events, or their continued effects, as we have seen in recent months.

The key point here is that if we think something is happening (such as the ongoing cost-of-living issues and rising tax costs), the markets have usually factored in the effects. Looking at the markets on 05 August 2026, in comparison to a year ago, we find the following (approximate) for a range of market indices:

The tax year 2026/2027 is well underway and the international football continues

As noted above, we are now well into the new tax year (2026/2027), with renewals of annual allowances where applicable; a good time to take a look at your overall financial planning as the summer continues, noting it’s been a very hot start and middle. Let’s hope it cools a bit soon.

We look forward to helping you with your financial planning and hope you continue to enjoy the summer and all it holds.

Keith Churchouse FPFS

Director

CFP Chartered FCSI

Chartered Financial Planner

Chapters Financial Limited is authorised and regulated by the Financial Conduct Authority, number 402899